In this blog post, we will explore the differences between variable and fixed interest rates on personal loans. We will discuss the pros and cons of each type and help you make an informed decision when choosing the right loan for your needs.

Variable and Fixed Rate

When you are in need of financial assistance, personal loans can be a great option. However, before you apply for a loan, it’s important to understand the different types of interest rates available.

In this blog post, we will focus on the two main types: variable and fixed interest rates.

Variable Interest Rates:

A variable interest rate is one that fluctuates over time based on changes in the market.

This means that your monthly loan repayments may vary throughout the loan term.

Pros:

Potential for lower interest rates: If market interest rates decrease, your loan repayments may also decrease, resulting in potential savings.

Flexibility: Variable-rate loans often come with flexible repayment options, such as the ability to make extra repayments or pay off the loan early without penalties.

Cons:

Uncertainty: Since variable rates can change, it can be challenging to predict how much you will be paying each month, making budgeting more difficult.

Risk of higher repayments: If market interest rates rise, your loan repayments may also increase, potentially putting a strain on your budget.

Fixed Interest Rates:

A fixed interest rate remains constant throughout the loan term, regardless of changes in the market.

Pros:

Certainty: With a fixed-rate loan, you know exactly how much you will be paying each month, making budgeting easier.

Protection against rate increases: If market interest rates rise, your loan repayments will remain the same, providing stability and peace of mind.

Cons:

Potentially higher interest rates: Fixed-rate loans often have slightly higher interest rates compared to variable-rate loans, as they include a premium for the stability they offer.

Limited flexibility: Fixed-rate loans may have restrictions on making extra repayments or paying off the loan early, which can be a disadvantage if you want to save on interest.

Choosing the Right Loan:

When deciding between a variable- or fixed-rate loan, consider the following factors:

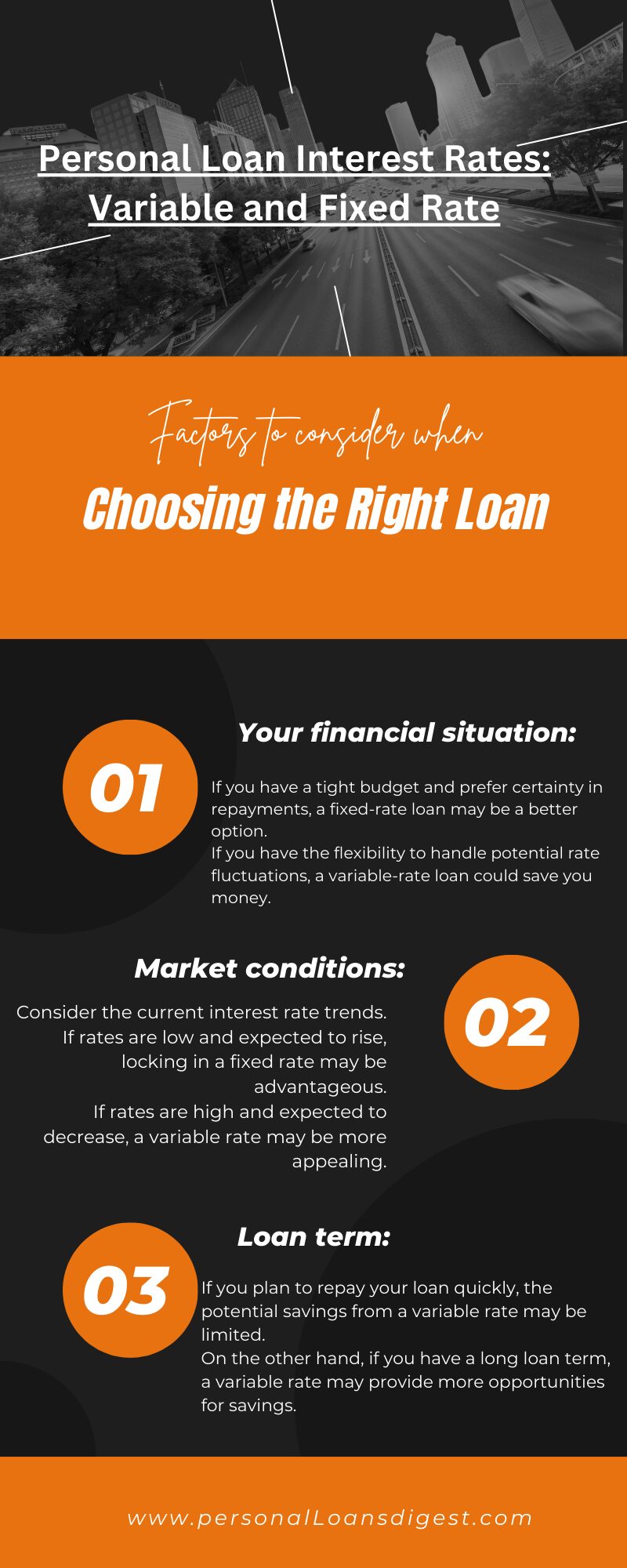

1. Your financial situation:

If you have a tight budget and prefer certainty in repayments, a fixed-rate loan may be a better option.

If you have the flexibility to handle potential rate fluctuations, a variable-rate loan could save you money.

2. Market conditions:

Consider the current interest rate trends. If rates are low and expected to rise, locking in a fixed rate may be advantageous.

If rates are high and expected to decrease, a variable rate may be more appealing.

3. Loan term:

If you plan to repay your loan quickly, the potential savings from a variable rate may be limited.

On the other hand, if you have a long loan term, a variable rate may provide more opportunities for savings.

In the end, the choice between a variable or fixed-rate personal loan depends on your individual circumstances and preferences.

Consider your financial situation, market conditions, and loan term to make an informed decision. Remember to compare different lenders and loan offers to ensure you get the best deal.